Improvement

Break-Even Point (BEP)

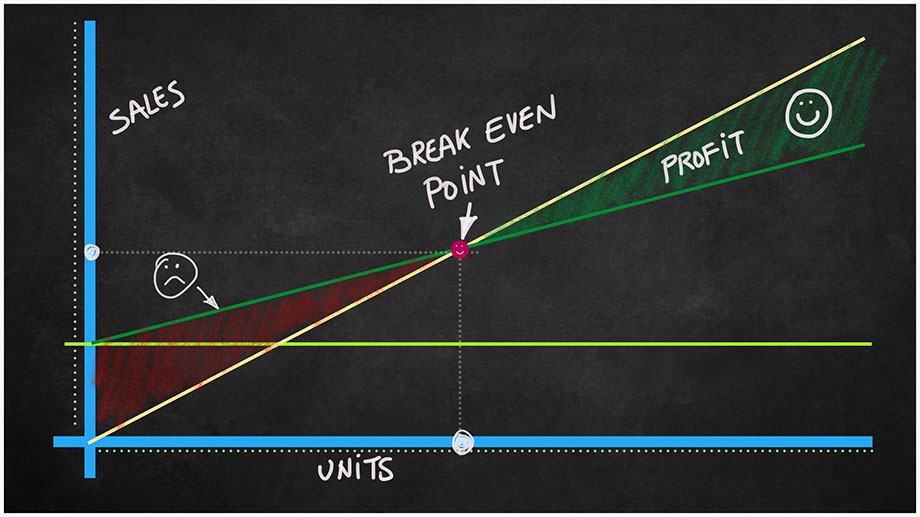

Definition: The Break-Even Point (BEP) is the point at which cost or expenses and revenue are equal: there is no net loss or gain, and one has "broken even." A profit or loss has not been made. (Wikipedia.com).

Importance: The BEP tells an owner the amount of revenue needed to cover all expenses, including fixed costs. The BEP, if used correctly, may help the owner to control fixed costs and/or to know the point of time in the future to incur more fixed costs.

Fixed costs: Examples of fixed costs include insurance, interest expense, property taxes, utilities expenses, rent and depreciation of assets. Also, if a company pays annual salaries to its employees irrespective of the number of hours worked, such salaries must be counted as fixed costs. (Investopedia.com)

Another benefit: Another benefit of the BEP might be in the specific identification of certain products or services that might either significantly add to or take away from a company's BEP.

Required: Accurate and timely financial statements are a minimum requirement to calculate a company’s break-even point. The balance sheet must be very accurate, even though the BEP is focused on the company's income statement.

Variable costs: Variable costs fluctuate directly with sales volume, such as purchasing inventory, shipping and manufacturing a product. (SBA.gov). A variable cost is a corporate expense that varies with production output. Variable costs are those costs that vary depending on a company's production volume; they rise as production increases and fall as production decreases. Variable costs differ from fixed costs such as rent, advertising, insurance and office supplies, which tend to remain the same regardless of production output. (Investopedia.com).

Total costs: Fixed costs and variable costs comprise total cost. (Investpedia.com).

Practical application #1: Imagine a business owner seriously pondering adding fixed costs to the company, such as the purchase of computer hardware, equipment, vehicles or adding salaries that would be considered fixed costs. That owner might consider the calculation of the BEP for these additional costs to see the additional revenue that would be needed to cover these costs. This process might take away some of the "guesswork" by the owner when making important decisions on fixed costs.

Practical application #2: Imagine a business owner sitting across the table from a key vendor. The key vendor gives the owner some "bad news" and explains that the cost of their product or service will increase by 5% beginning next month. The owner might consider the impact to the BEP before agreeing to the increased costs. This increased "variable cost" might require the sales of the company to increase to a certain amount in order to break-even. The owner has the right to know the amount of the increased sales needed and the costs, if any, of obtaining those increased sales.