Acquire a Company

To Increase Market Share

Good news: It is possible for your company to increase its market share by the acquisition of another company.

Bad news: With rare exceptions, the financial information of the seller is incorrect. It then becomes very difficult to put a correct value on the seller until such financial information is correct and until a certain amount of due diligence is performed. The due diligence should be performed in a way that satisfies any concerns your company may have about the seller.

Due Diligence: Due diligence is an investigation of a potential investment to confirm all facts, such as reviewing all financial records, plus anything else deemed material. Due diligence refers to the care a reasonable person should take before entering into an agreement or a financial transaction with another party. When sellers perform a due diligence analysis on buyers, items that may be considered are the buyer's ability to purchase, as well as other elements that would affect the acquired entity or the seller after the sale has been completed. (Investopedia.com).

Purpose: The purpose of due diligence on the part of the buyer is to validate the information provided to a point where the buyer feels reasonably comfortable and understands the risks involved in the purchase. In virtually every transaction, the buyer's offer is contingent upon the results of the due diligence process. (John F. Dini, quoted in The Exit Strategy Handbook, fourth edition, p. 70).

Seller reactions: Most owners are shocked by the depth and breadth of the due diligence process. This process of "full and fair" disclosure enables a buyer to verify all provided data and reviews all information about the company. "All" includes anything that would interest the buyer at any level. Most business owners are highly independent people who find this disclosure process extremely uncomfortable. (John Brown & Kevin Short quoted in The Exit Strategy Handbook, fourth edition, p. 73).

Comprehensive: Both buyers and sellers are often stunned at the comprehensive nature of a correct due diligence process. Most feel that the process is limited to looking at financial information and tax returns. As is disclosed on the table of contents of The Exit Strategy Handbook, fourth edition, financial and tax information represent only four (4) of 18 different categories that should be considered when performing due diligence on a company to be acquired. For the purchaser, some of the other 14 categories may be just as important, if not more so, than the financial information of the seller.

Risk: Most professionals will advise you to use outdated techniques, such as spreadsheets, to track the due diligence process. There is risk in giving this much control to any one person and by using old-fashioned software such as spreadsheets. It is not in your best interest to have the due diligence on one person's laptop, which can be lost, or even worst, stolen.

Control: A business owner must insist to be in control of the due diligence process. Otherwise, the owner loses control. The best way to keep control of the process is with dashboard software that has be created just for this purpose in order to keep the owner in control of due diligence at all times during the process. This software must be user friendly and allow the owner to keep control of the process 24/7/365 on a smartphone, tablet or computer.

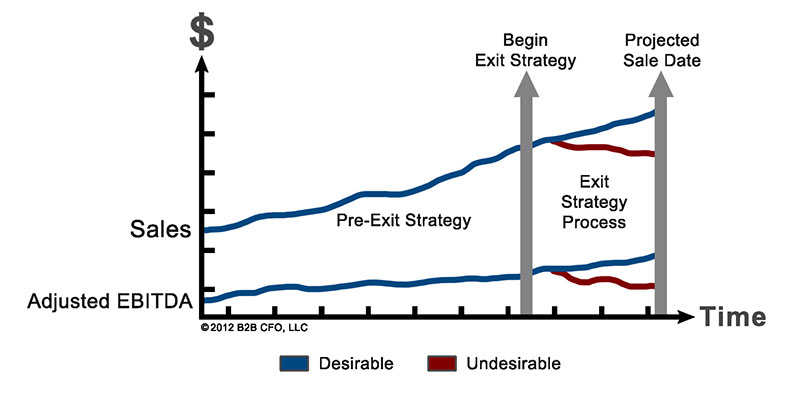

The seller: You want the seller to continue to grow their business, take care of existing customers, vendors and to acquire new customers. In short, it is in your best interest to have the company you are buying to continue to grow in value. Unfortunately, too many sellers get distracted during the due diligence process. They often get in "the weeds" of the detail or simply stop running the business in a growth mode. It may be in your company's best interest to have the seller follow the process in the graph below during the due diligence process.

Audits: The business you are acquiring may or may not have examinations by independent CPAs on their financial statements. If not, you and your Exit Team (The Success Team™) will want to decide if it is in your company's best interest to have an audit (or Review) by an independent CPA firm. The cost of paying the fees to the CPA firm is a topic of negotiation between the buyer and seller.

Tax returns: Is the seller current with all tax return filings, including federal, state, sales, use, payroll (Federal withholdings, state withholdings, FICA, FUTA, Medicare, Medicaid, etc.), franchise, etc.? Have there been any rulings or concessions that have been obtained from any domestic or foreign governmental agencies? Are there any current ongoing audits by domestic or foreign governmental agencies? Are there any actual, anticipated or potential challenges to the seller's tax treatment (e.g., income, franchise, personal property, real estate, sales, use, payroll withholdings, etc.)?

Havoc: Audits can wreak havoc on a deal for two reasons. First, if not properly prepared for, they can add two to four months to the length of a deal. Second, audits provide the buyers with a host of reasons to lower the price. (John Brown, quoted in The Exit Strategy Handbook, p. 149).

Checklists: Below are some of the checklists your company should consider when purchasing another business.

- General Information

- Management and Employees

- Product and Service Lines

- Competition

- Customer Information

- Key Vendors and Service Providers

- Intellectual Property and Intangible Assets

- Technology, Software and Hardware

- Branding, Marketing and Public Relations

- Related Parties and Minority Shareholders

- Insurance

- Internal Financial Information

- Inventory

- External Financial Statements

- Contracts and Leases

- Litigation and Claims

- Taxes

- Environmental